First, a big thank you to everyone who responded to my RealDataSF Poll about how to make this newsletter better. This month’s topic is a direct result of your input, as information about tax-related topics was among the top 3 subjects my readers wanted me to cover in addition to market news (the other two were investing in and renovating property).

Some other quick results:

- 92% of responders found the length of my newsletters “about right.”

- 72% thought the amount of data was “perfect”; 24% wanted more; 4% wanted less.

- 58% were fine with occasional newsletters on more personal subjects.

- 68% forward my newsletter “occasionally;” 4% share it “all the time; and 28%, “never.”

- Several people wrote that it’s the “best real estate newsletter out there.” (Thank you!). One suggested that “Haikus in Latin would be a great addition.” (Working on it!)

For those who didn’t receive the poll or who would still like to respond, you can access it by clicking here.

____________________________________________________________________

Now on to taxes. Let’s get the disclaimer out of the way: I’m not an accountant or a tax attorney and I’m not giving tax or investment advice. These issues are complicated and the rules are ever-changing so go see a real expert. My purpose here is simply to identify some of the main tax subjects you should be aware of if you own residential property. Whew!

Excluding Tax on Capital Gain from the Sale of Your Home

If you have a capital gain from the sale of your home, you may be able to exclude up to $500,000 of that gain from your income if you are married and filing jointly (or $250,000 if an individual), provided that you have owned and lived in the home as your principal residence for an aggregate of at least two out of the five years before the sale.

What’s “capital gain?” It’s often misstated as simply the difference between what you bought your house for and what you sold it for. In reality, “capital gain” is more complicated than that but will usually result in a smaller potentially taxable net gain, which is always good.

“Capital gain” is the home’s selling price minus deductible selling costs (which include brokers’ and escrow fees) and minus your “tax basis” in the property. Your “tax basis” is what you paid for the property plus some of the costs of acquiring it, plus major improvement costs you’ve incurred during your ownership, so it’s worth keeping track of them. The best explanation I’ve found for this tax benefit is at Nolo Press’s excellent website, here. You can also take a look at the IRS’s info pamphlet here.

There’s no limit on the number of times you can use this exclusion, provided that you meet the 2 year ownership and use minimums each time you claim the exclusion. Some serial flippers buy a home, live in it for a couple of years while they fix it up, sell it, buy a new one and start again.

Escaping The “Golden Handcuffs” of a Low Property Tax Assessment: Prop 60 and 90

Empty-nesters and other long-time home-owners often think about selling their home and buying a smaller or more convenient one so that they can simplify their lives, live closer to family, or untap the home’s increase in value for other purposes (see “Excluding Tax on Capital Gain” above). What can stop them is that they may end up paying far more in annual property tax assessments even if they’re buying a more modest home.

How come? Under California’s Proposition 13, passed in 1978, property in California is reassessed when it’s sold, transferred, or substantial improvements made to it. Otherwise, the property is taxed at around 1% of the purchase price (with minor additions for locally approved bonds and levies) and then those taxes only increase by an inflation factor which cannot exceed 2% per year.

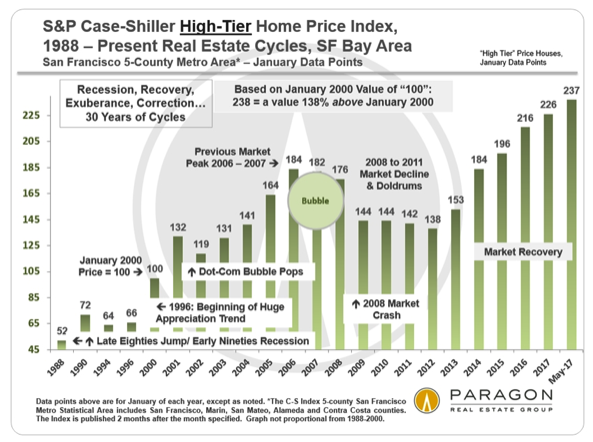

Consider that according to the widely followed Case Shiller Index, higher priced homes in the San Francisco Bay Area have have increased by a whopping 137% since January 2000 (ie they’ve more than doubled). Even assuming the maximum annual increase of 2% compounding per year, a homeowner’s property tax assessment would only have increased by about 40% over the same 17 year period.

Now, let’s say the home you bought for $500,000 in 2000 has increased by 138% and is worth $1.2 million today. Your annual property taxes, which started at around $5,000 are now about $7,000. You want to downsize and you have your eye on a nice little condo that you could buy for $800,000, allowing you to put some money away for your retirement. The problem? You’ll be paying $8,000 in property taxes on your new home – $1,000 more than on your old one – even though it’s worth $400,000 less.

Recognizing this problem, in 1986, California passed Proposition 60, which gave homeowners 55 or older a one-time right to transfer the property tax assessment on their existing primary residence to a new one purchased for no more than the sale price of their previous one, provided both homes were located in the same county. Two years later, Proposition 90 was passed. It allows qualifying homeowners to transfer their property tax assessment to new homes located within eleven counties that have agreed to reciprocal transfer rights. In the Bay Area, only San Mateo, Alameda, and Santa Clara participate, so San Francisco homeowners are currently out of luck.

That may change, however. According to a recent article, the California legislature is considering a bill that would permit assessments to be transferred between any county in the start, starting in 2019. This could be a huge boon for people looking to move to cheaper areas or simply to be closer to their families.

I’ll cover some additional tax subjects like 1031 exchanges in future newsletters. Thanks for sticking with me on this unusually lengthy one. And let’s see if we can increase my readership: please share my newsletters with others and “like” them on Facebook, Twitter and LinkedIN.

As always, your comments, questions, and referrals are very much appreciated!

Misha

Great read. Wonderful to come across a post with this kind of information. Thanks for sharing.