Back in May 2018, when pundits everywhere delighted in sounding the death-knell for SF’s residential market due to a host of local challenges including lack of affordability and rampant homelessness, I suggested they might be a bit premature. In the summer of 2020, months into the Covid pandemic, Zillow published data suggesting that SF was again on the skids. Again, I suggested that “this too shall pass.” Condo and home prices proceeded to hit record highs until 2022 when higher interest rates brought the real estate party to a stop, leaving a hangover from which much of the Bay Area — indeed the country as a whole — has yet to recover.

Interest rates are still high, albeit with indications that they may be coming down “any day now.” Add in such challenges as the economic uncertainty engendered by Trump’s tariff wars; an enduring change in the remote/on-site work model; and a persistent narrative of SF’s “doom loop” decline, and it’s fair to ask whether SF can once again pull off a Houdini-like escape.

There are signs, if tentative, that it might, and this time the “key” will be the AI Revolution.

SF vs. The Rest of the Bay

In our August Market Report, our whizz-bang market analyst, Patrick Carlisle, states that “Unlike most other markets, [SF’s] supply of listings is dropping, price reductions are declining, and home prices are starting to climb year-over-year.”

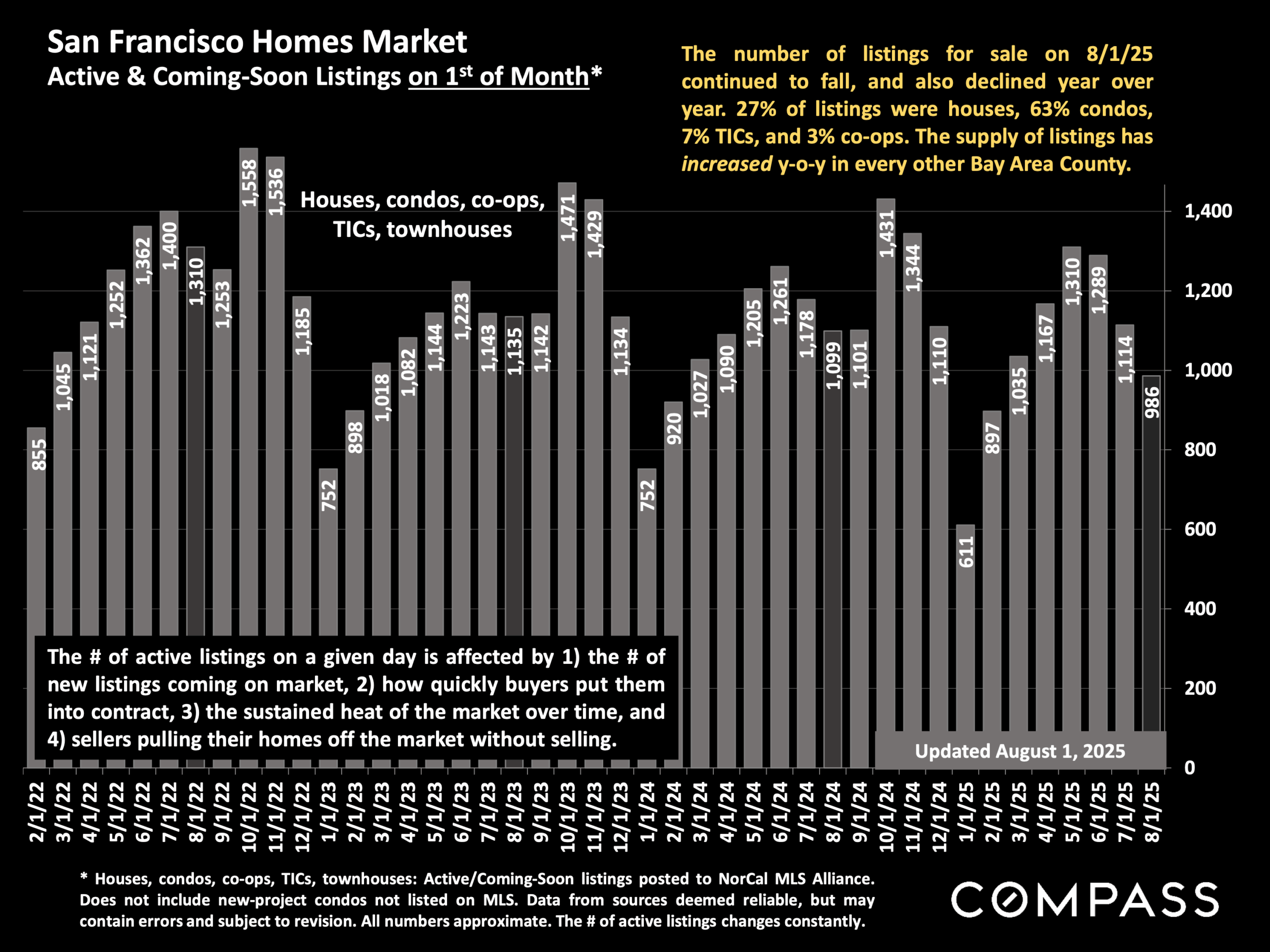

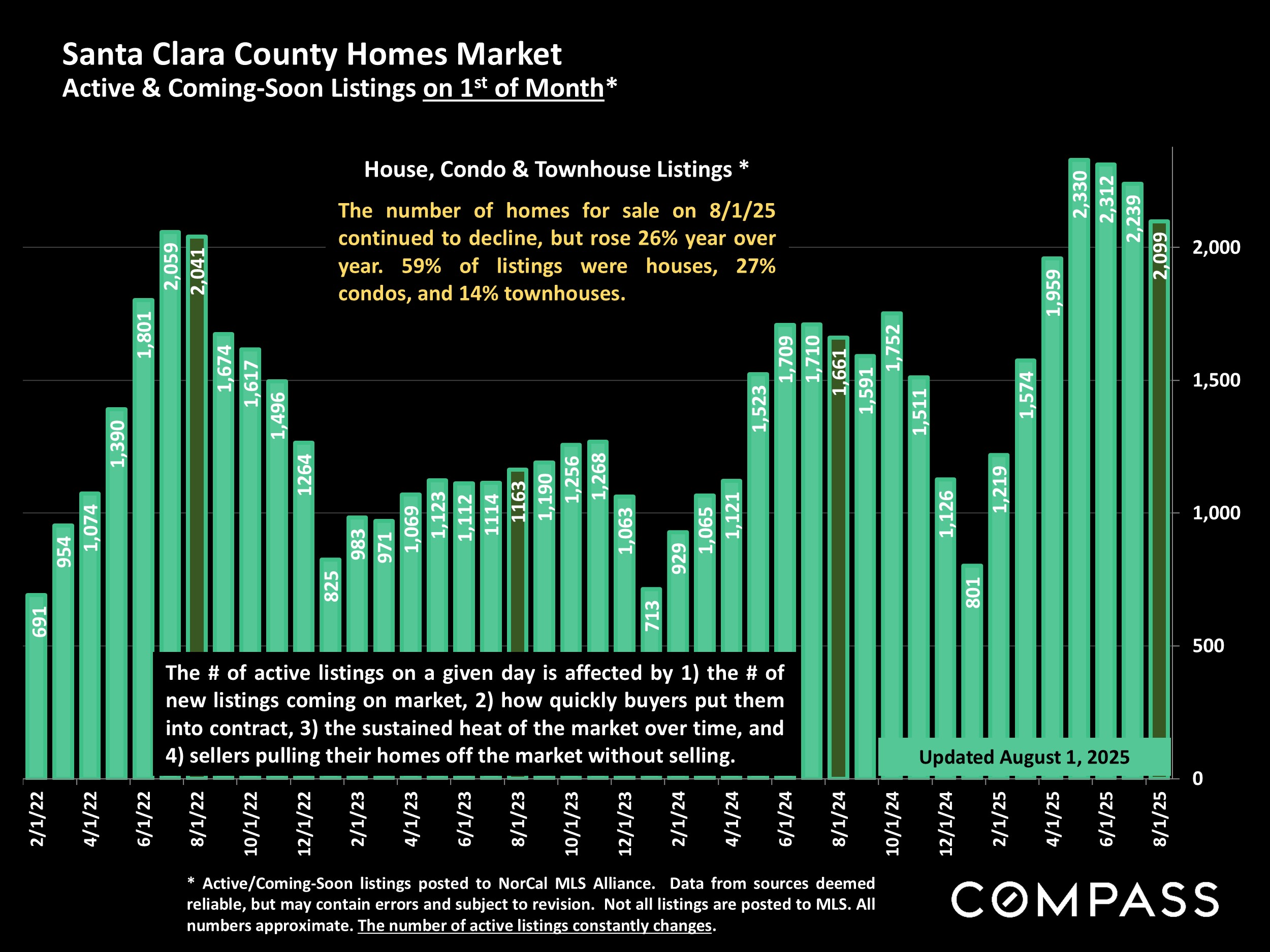

On the supply side, active and coming-soon listings for August have declined year over year, and every year, since 2022. While the number of listings on the market has a definite seasonal component, as reflected in the regular peaks and troughs visible in the chart below, the downward trend is the opposite of what is happening in other Bay Area Counties. Even Santa Clara County, which profits from the AI boom with the likes of Nvidia headquartered there, has shown consecutive annual increases in listings available (second chart).

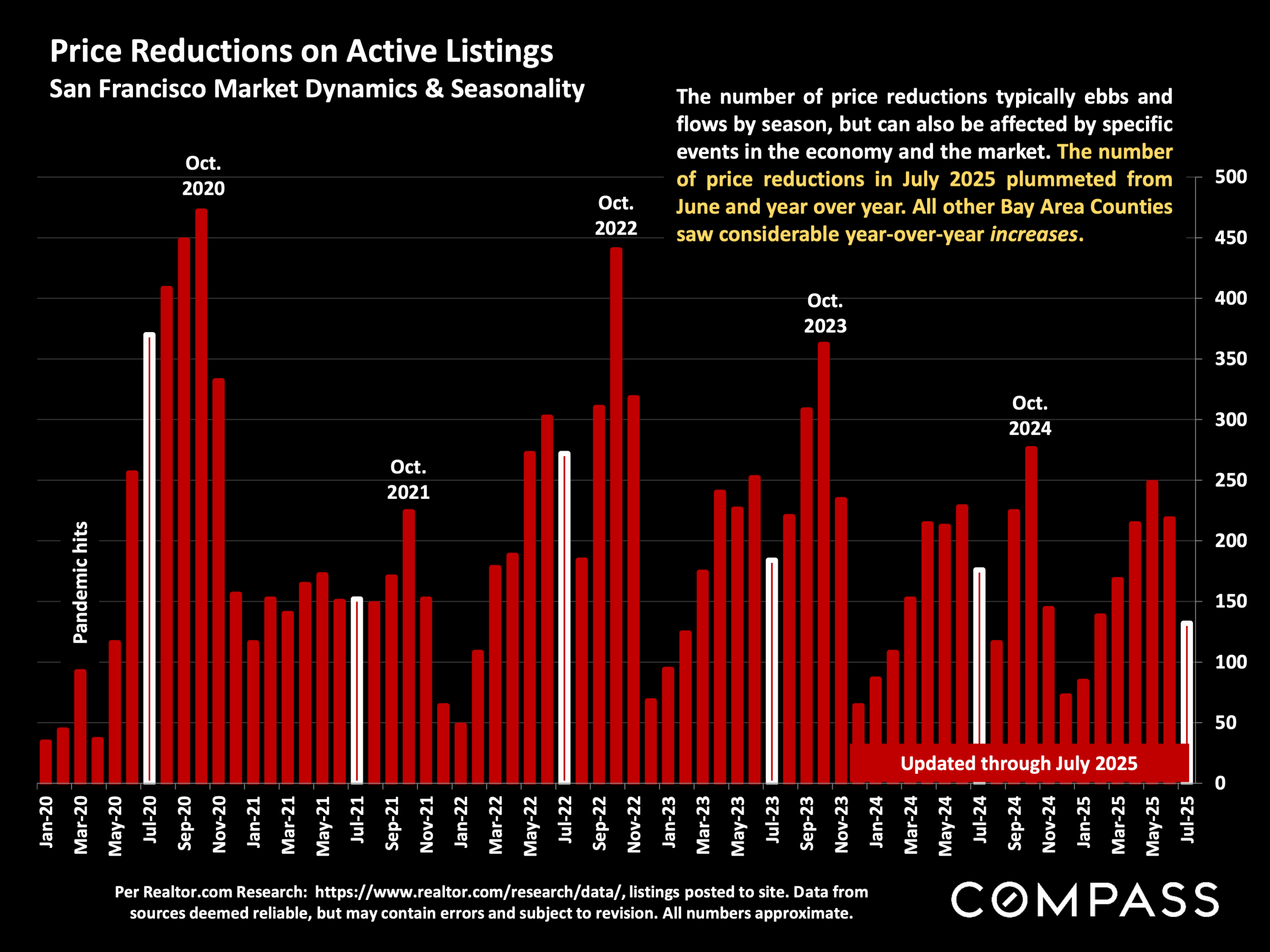

Another sign of SF’s strength relative to the Greater Bay Area: price reductions on active listings. For July, SF posted a significant decline in these from a year earlier. All other Bay Area Counties saw “considerable” increases.

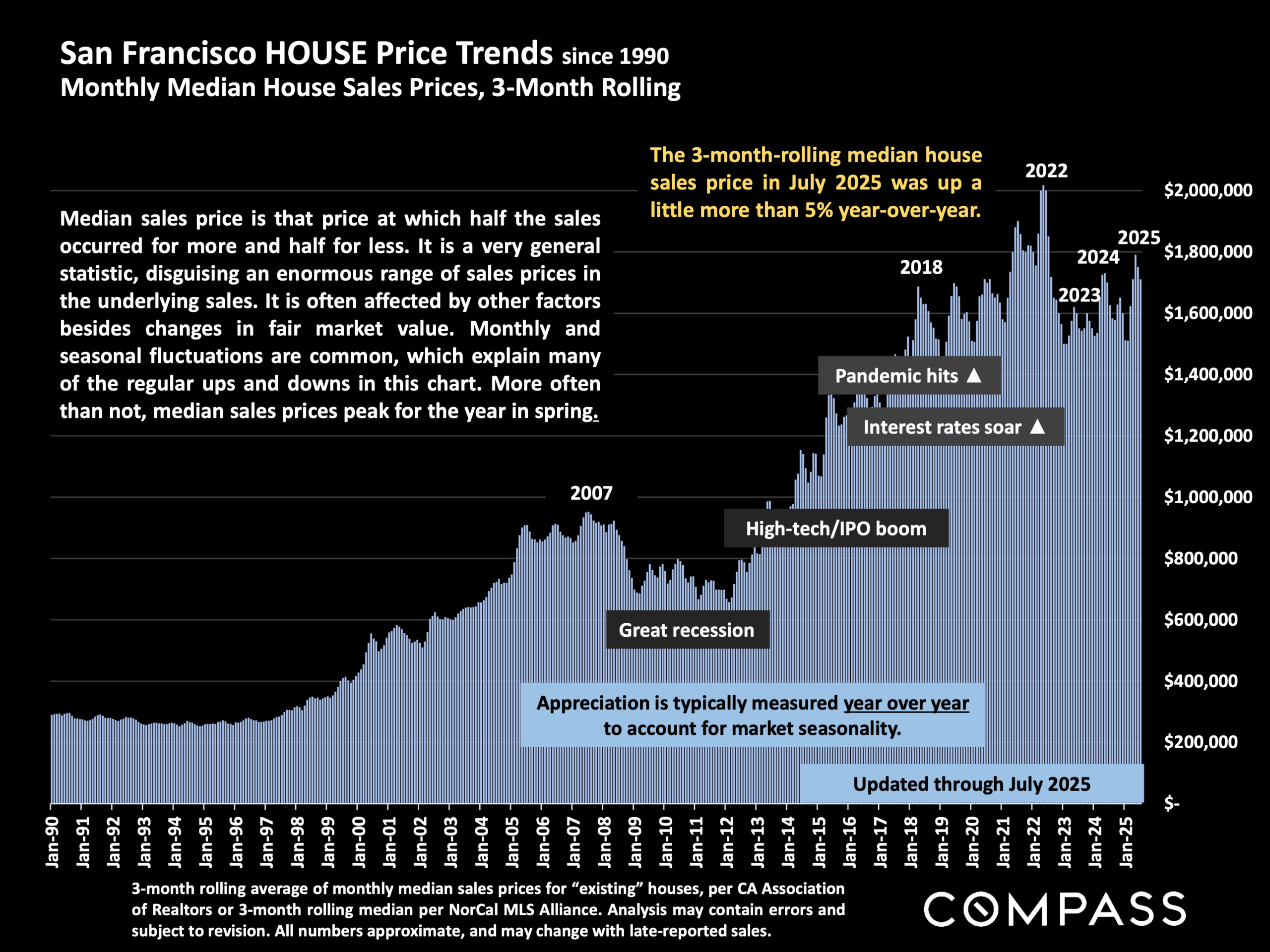

House Prices: Some Positive Signs

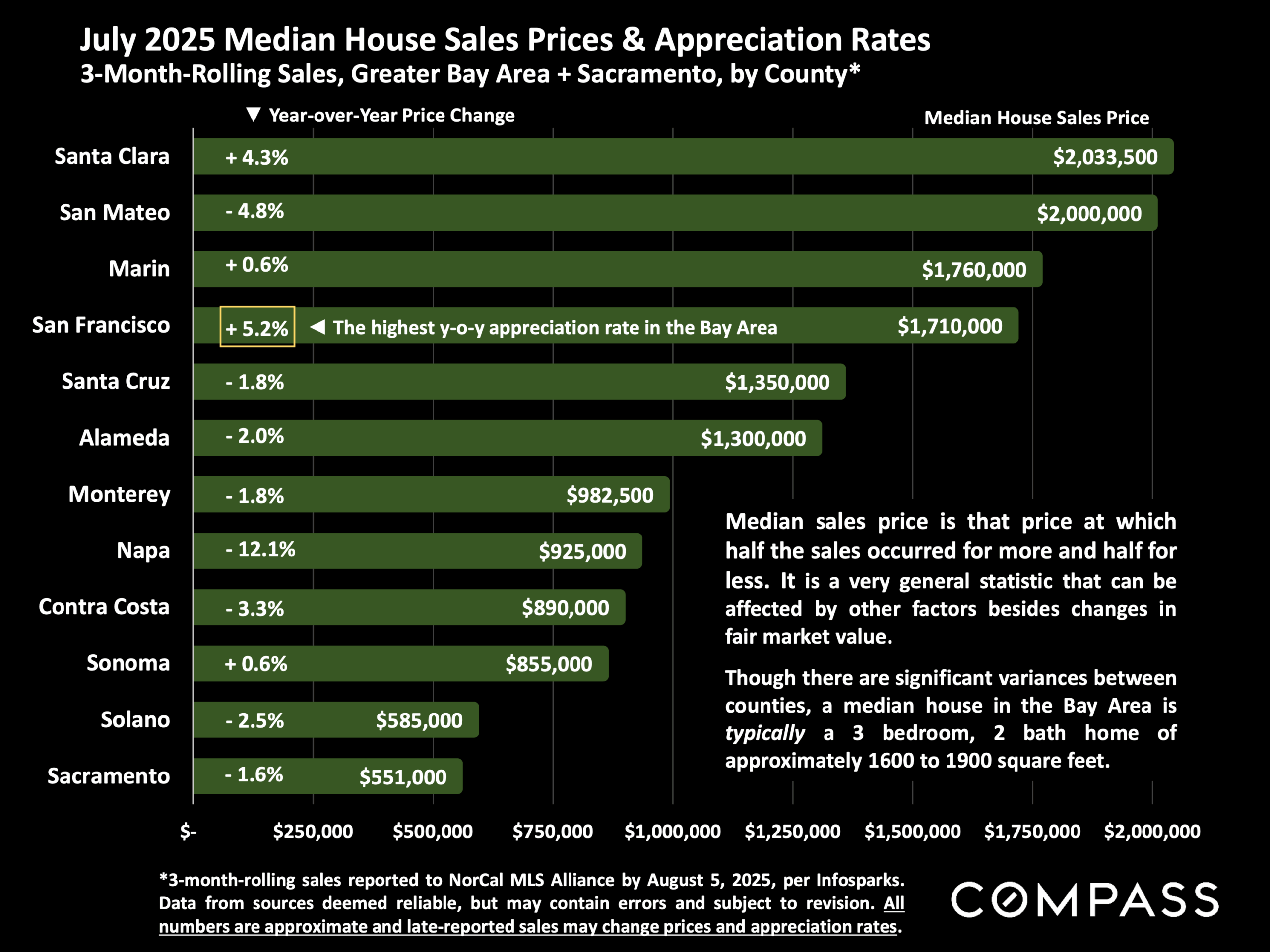

Given the constrained supply and fewer price cuts, you’d expect upward pressure on home prices. Looking at the first chart in this newsletter, it’s hard to see much of a “trend” yet, though house prices were up 5% in July Y-O-Y. Perhaps more indicative of growing strength in SF’s market is, again, how it compared to other counties (chart below). Here, SF led the way with the highest Y-O-Y appreciation (5.2%). Santa Clara was the only other county posting significant appreciation (4.3%). All other counties except Sonoma posted declines. Still, at a median house price of $1,710,000, we are still well below the January 2022 peak of just over $2 million.

The AI Effect

If AI money is having an effect on the market, this is exactly where you’d expect to see it: in (relatively) strong single family home sales in the two counties – SF and Santa Clara — where this industry is concentrated. Just two AI companies headquartered in SF, Open AI and Anthropic, have together raised over $45 billion so far this year, with Anthropic poised to raise another $5b. As of Q1, those two companies alone had raised almost half of the total amount of VC funding in AI. As a more recent article in the Washington Post put it, “the Bay Area is home to the largest venture capital investments in the AI industry by far.” The same article quotes Nvidia’s CEO Jensen Huang as saying: “It’s because of AI that San Francisco is back…. Just about everybody evacuated San Francisco. Now it’s thriving again.”

Not Just Homes – Luxury Homes

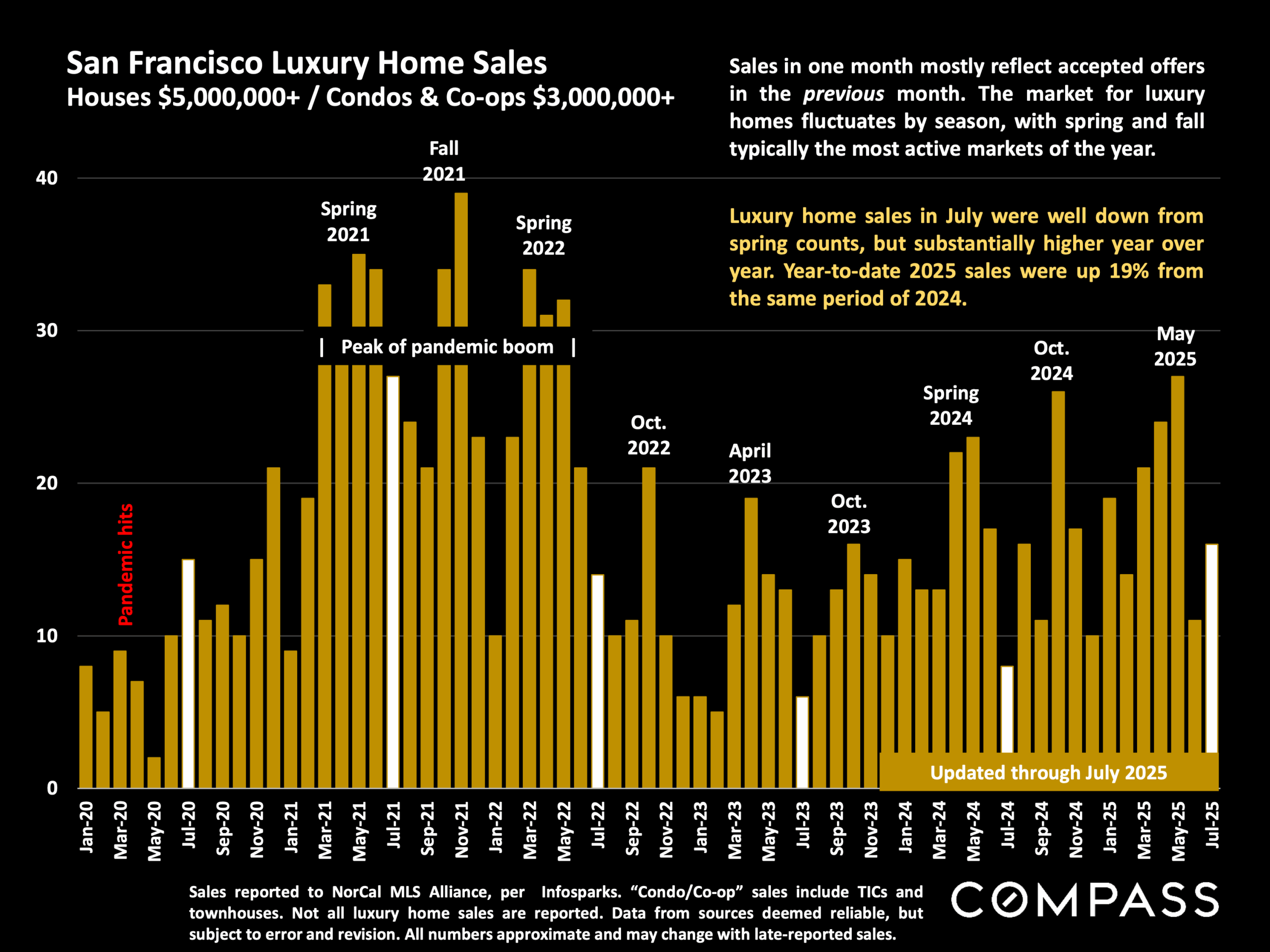

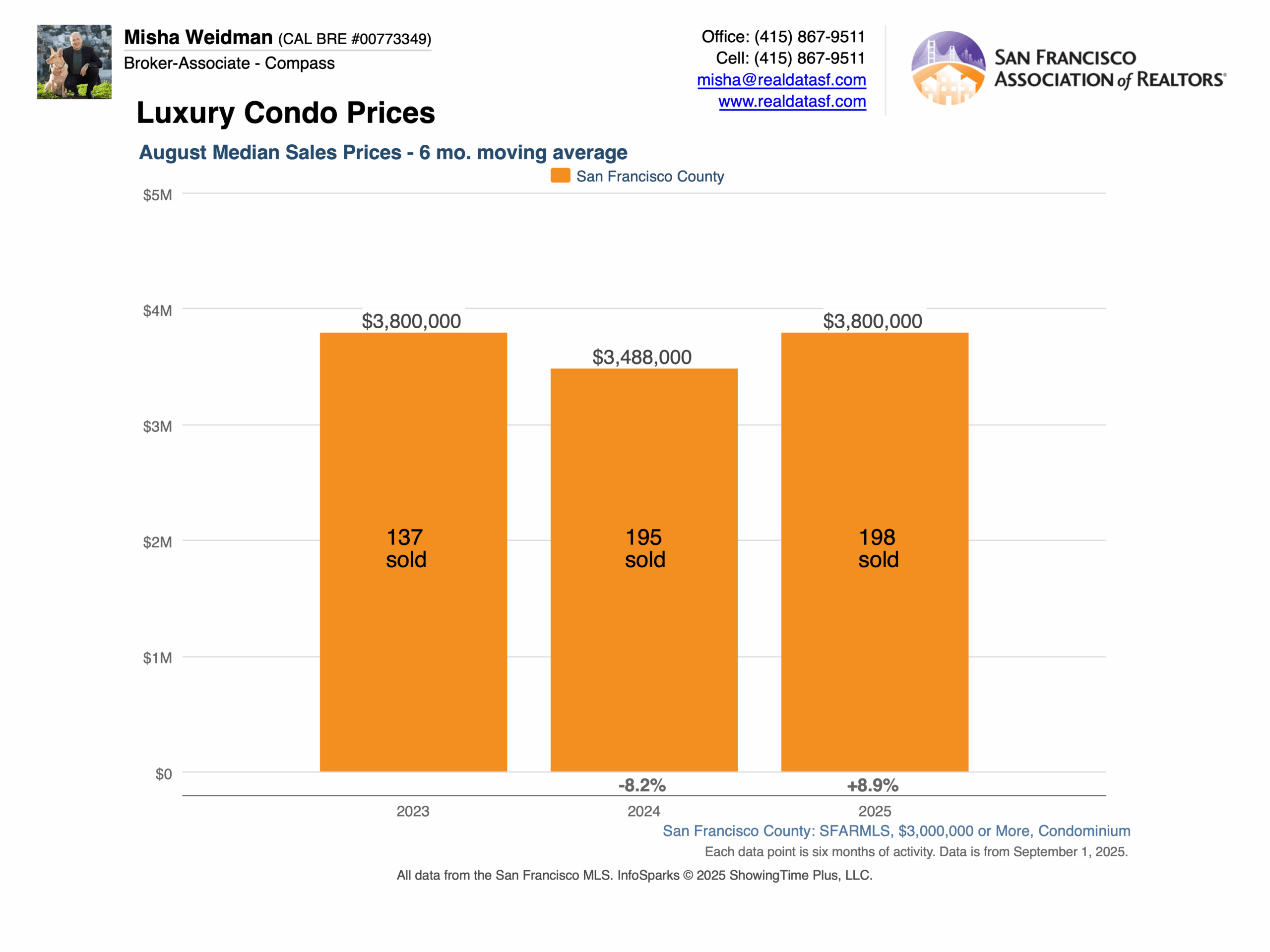

And of course, between record signing bonuses, high salaries, and liquidity provided by secondary sales, well-placed employees in AI startups and others have the funds to be able to afford SF’s priciest homes. Sure enough, the luxury home market is very active. July 2025 luxury home sales — those over $5 million for houses and $3 million for condos — were up 19% Y-O-Y (chart). (Luxury sales volume typically slumps during the summer months, so the fact that numbers are well down from May is likely just seasonal.)

And sales prices, as well as volume, tell the same story. Both luxury houses and condos are easily outpacing their less affluent cousins.

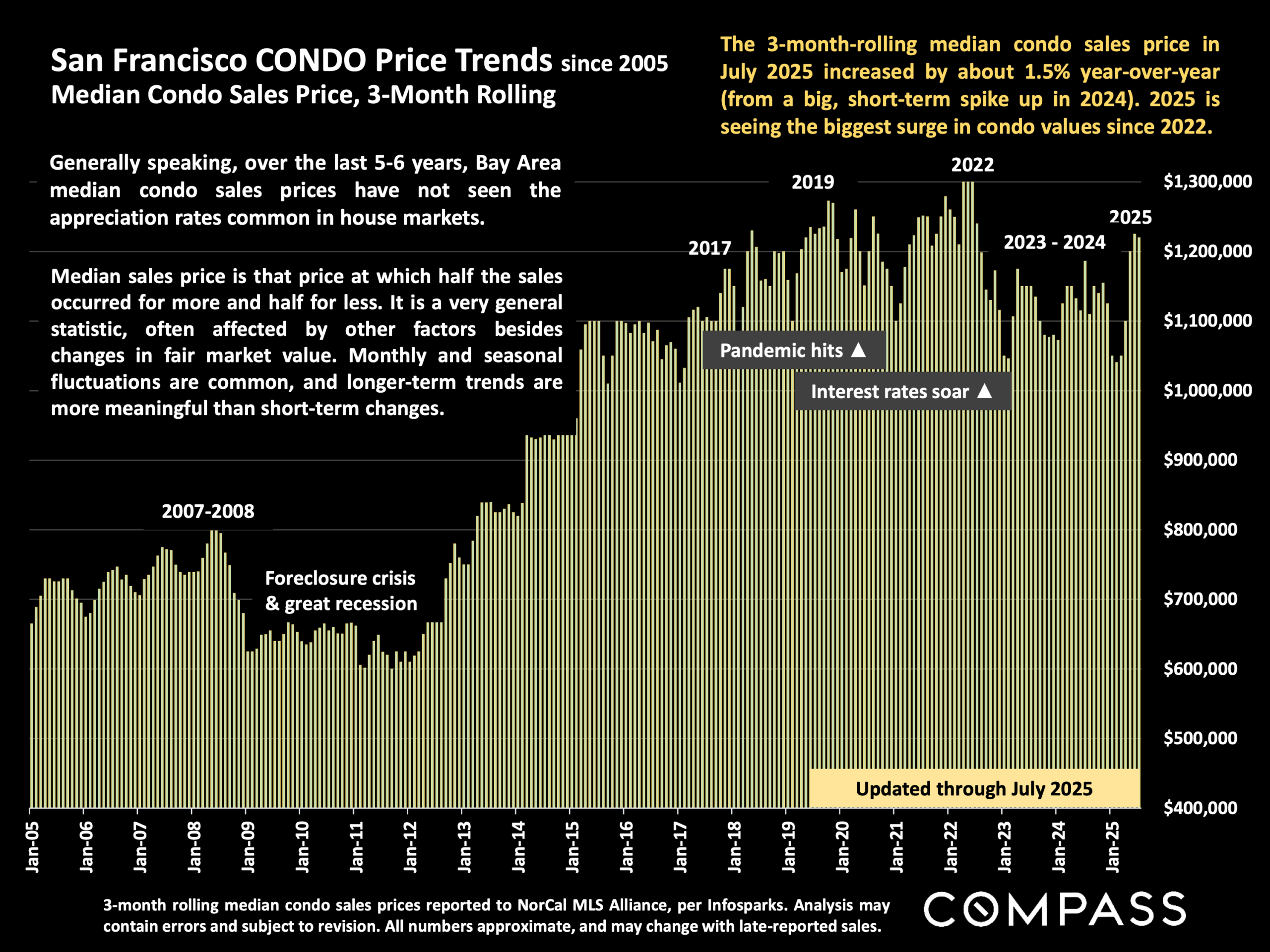

Condominiums: The Canary in the Coal Mine?

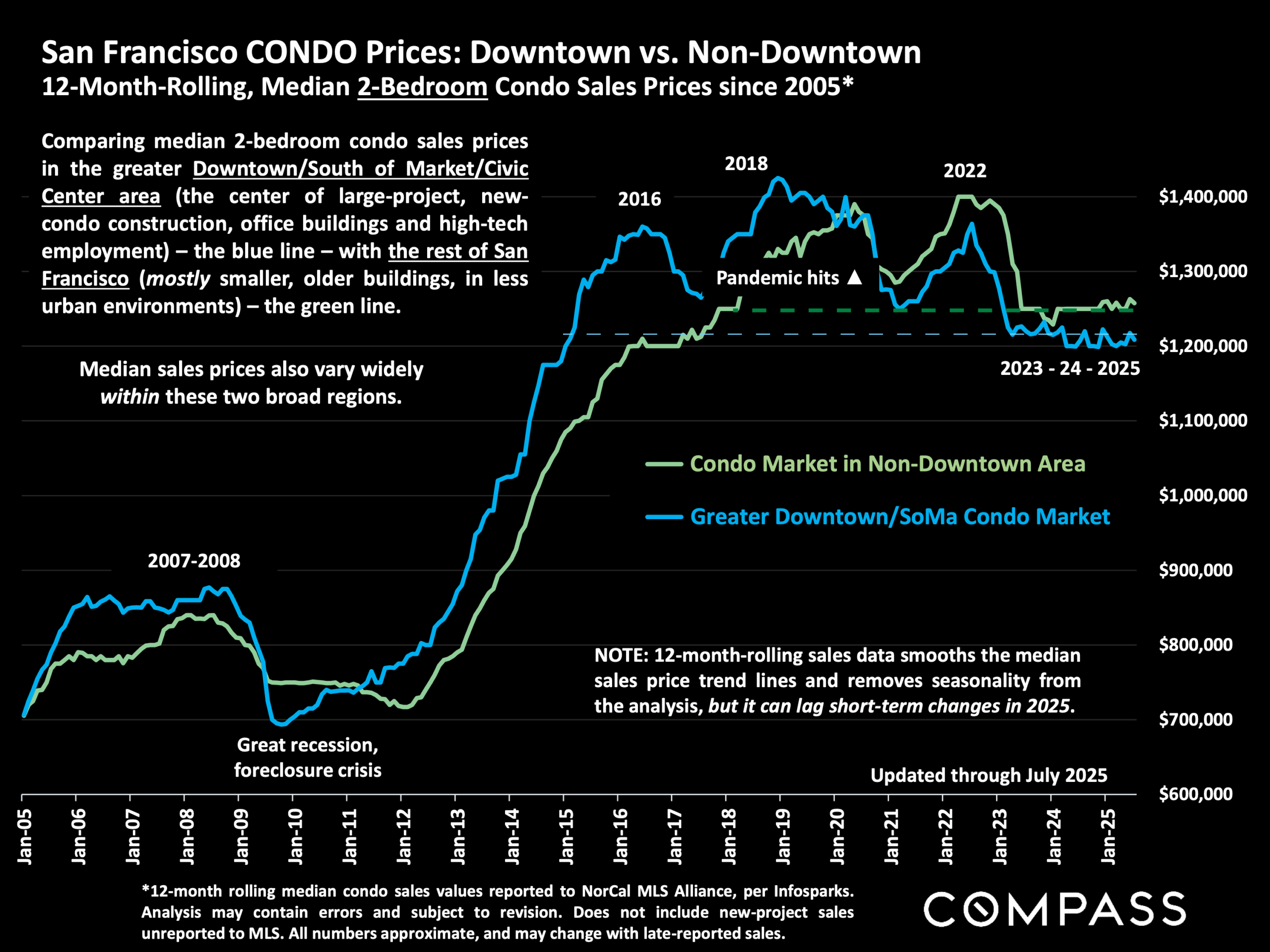

Condominiums have always been more sensitive to market forces than single family homes. And in SF, we’ve had two geographic markets, broadly speaking: condos in newer high-rises in the downtown/South of Market area (SOMA) and condos in generally older, smaller buildings in SF’s neighborhoods. Condos in SOMA really took the brunt of the exodus from the city following the Covid-19 outbreak. While condos outside of SOMA fully recovered within a few years after the pandemic, condos within SOMA never got back to their 2018 highs (chart below). With interest rate hikes from the Fed’s tightening monetary policy starting in 2022, condo values everywhere slumped again. SOMA condos have been stuck at roughly 2015 values; non-SOMA condos are back down to 2018 values.

Still, there may be signs of improvement. While the 3-month-rolling median sales price for all condos in July 2025 only increased by about 1.5% against an unusual data spike a year earlier (second chart from top), our typically cautious chief market analyst, Patrick Carlisle, states that “2025 is seeing the biggest surge in condo values since 2022.” Maybe, but when I stripped out sales of condos above $3 million, I found a slight decline in year over year sales price, so I wonder whether the overall increase is due to those luxury condo sales I discussed previously.

Glimmers

Beyond our stats on the residential sales market, there are other positive signs for San Francisco’s recovery. Over the last 12 months, rents in SF are rising at the fastest rate in the country, according to SF’s July Status of the Economy. Downtown foot traffic is also up, according to the same report. And AI companies are occupying a whole lot of downtown office space too. Perhaps we are not yet, as Nvidia’s Huang put it, “thriving again,” but I too feel that there’s new energy in town. In hipster neighborhoods like Hayes Valley, the Marina, the Castro and Valencia Corridor, you can see crowds once again spilling out of bars and restaurants – a remarkable change from just a year ago. While “recovery” brings its own challenges, including affordability, traffic, and an increasing divide between the haves and have-nots, signs of life returning to the city surely can’t be a bad thing.

….

It’s been a while since I last published a newsletter. I’ll offer no excuses. Over the years, I’ve gotten great feedback from my readers in the form of emails, texts, and even the occasional phone call. I’d love to hear from you! As always, your comments, questions, and referrals are much appreciated!

As always a splendid analysis and thoughtful perspective, Thanks!