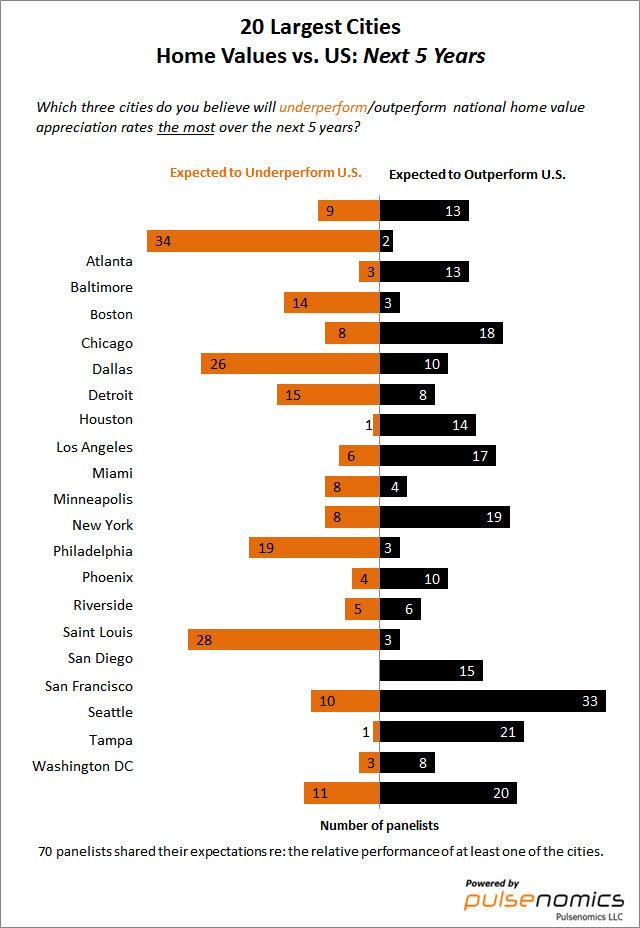

Just a few days ago, The San Francisco Business Times reported that a third of the national housing experts surveyed by Zillow described the Bay Area’s housing market as being currently in a bubble. Here’s the table that shows how the experts came out on the “bubble” question, courtesy of Pulsenomics, who conducted the survey for Zillow.

Just a few days ago, The San Francisco Business Times reported that a third of the national housing experts surveyed by Zillow described the Bay Area’s housing market as being currently in a bubble. Here’s the table that shows how the experts came out on the “bubble” question, courtesy of Pulsenomics, who conducted the survey for Zillow.

On the one hand, you could say that a lot of experts feel that, if San Francisco is not already in a bubble, there’s a “significant risk” that it will be in one within the next 1 to 5 years. At the same time, San Francisco ranks at the top of the experts’ list for cities likely to outrank national home appreciation rates by the most over the next five years.

Hmmm. Technically, those two conclusions – bubble and out-performance – might not contradict each other, but they certainly seem to be inconsistent with the notion of an imminent pop.

Here’s the takeaway: I don’t think there’s much of a takeaway.

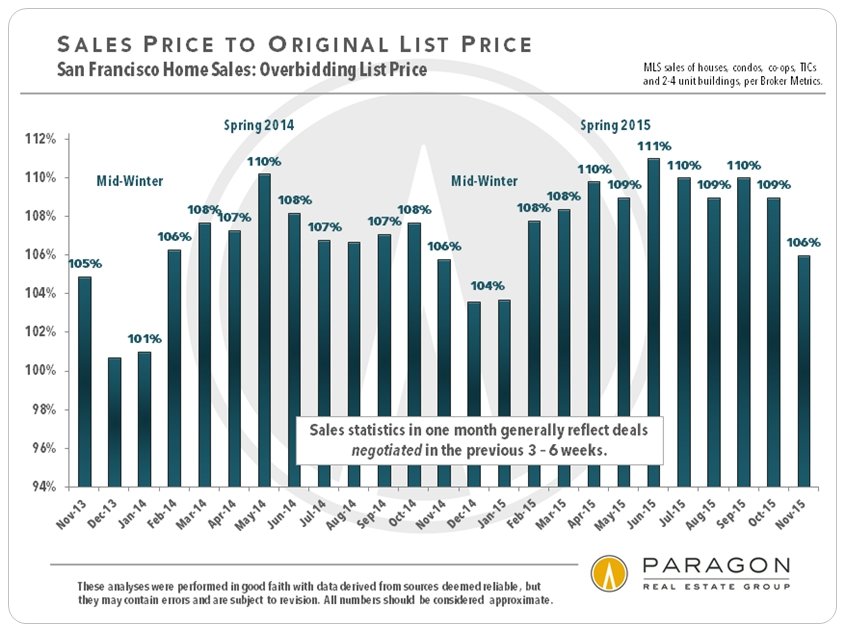

Certainly, 2015 was another very strong year for San Francisco real estate. Of course this merely begs the question as to what the future holds. The next few charts show where we are, heading towards the end of the year.

By the broadest measures, prices have continued to move up and there has been no drop in the percentage above list price that buyers have been paying. True, these statistics reflect transactions that occurred three to six weeks earlier, but after looking at a number of metrics on inventory, sales, and pricing, I was only able to find one metric that might indicate a softening trend, and that’s the number of sales taking place.

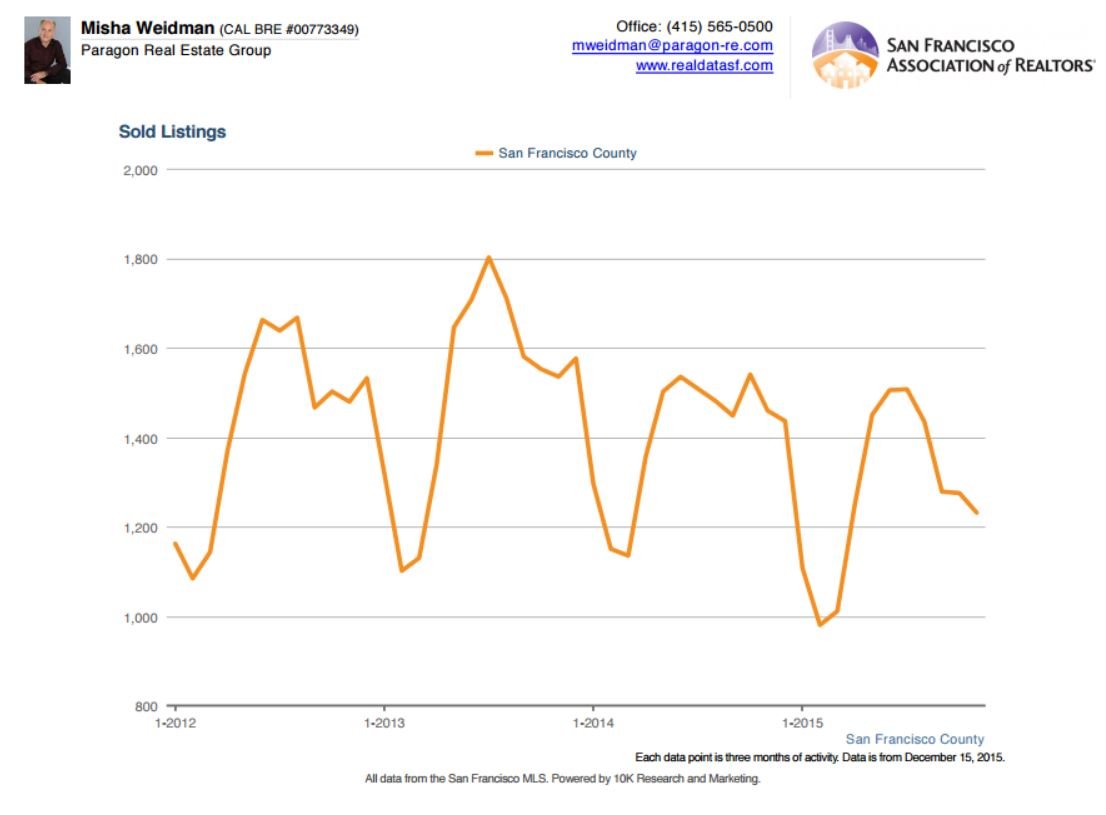

The chart shows total sales based on a rolling 3 months basis. You can easily see the seasonal drop-off in sales during the winter months, as well as the seasonal dip during the summer. What’s different in 2015 is that sales activity didn’t look like it came back after the summer dip.

For example, in September 2014, there were 1,448 sales (3 month rolling average); in September 2015, there were 1,275. That’s a 12% drop in sales. The drop in year over year sales for November 2015 was over 15%.

The number of sales alone doesn’t tell us anything about the dynamic between supply and demand; for that, a better measure would be Months’ Supply of Inventory, which we looked at in last month’s newsletter. However, the slower rate of sales accords with my and other agents’ current experience “on the street” — and that is: the market’s slowing.

Considering how much prices have gone up over the last few years, that wouldn’t be a bad thing. Through November 2015, the average sales price for single-family homes is up 12.3% over the previous 12 month period, even outpacing the 11.8% gain seen in 2014. Condos also scored double-digit gains over the last two years and beyond.

The Wild Card: Interest Rate Increases?

Everyone knows that interest rates are going to go up – finally. In the short term this might actually spur another feeding frenzy as buyers try to get into the market before further interest rate increases eat into their buying power. In the longer term, though, those rate increases might start weighing on the market unless balanced by a really strong economy that buoys buyer income.

Conclusion: Stay Tuned

People much smarter than I have guessed wrong over and over again on where markets – any markets – are headed. I’ll stick my neck out and say that SF seems to be transitioning to a more balanced, less buyer-driven market. I wouldn’t be surprised to see a spike in Spring 2016, but beyond that, prices could stabilize, especially at the higher end where we are already seeing the market soften.

As always, your questions, comments, and referrals are much appreciated!