“Home ownership has dropped, evictions and homelessness have climbed sharply, surging demand for rental units has led to a shortage, and soaring rents are fodder for daily conversation…. In the last few years, [it] has become one of the world’s 10 most expensive places to rent, ahead of cities like Tokyo, Sydney and Singapore.”

San Francisco? Actually, Dublin, Ireland, according to a Deutsche Bank Report cited in a New York Times article a few days ago. But before you heave a sigh of relief, consider this: Dublin ranked 8th most expensive city in the world to rent a mid-range 2 bedroom apartment, clocking in at around USD $2,000. San Francisco came in second – just after Hong Kong and ahead of New York. The quoted rent for SF: a whopping $3,631, down slightly from 2018.

And yet our currently foggy piece of heaven’s Quality of Life Index still ranks among the Top 10 for major global cities covered by the Report, clocking in at number 9. The only major U.S. City that does better is Boston, at number 8. (New York ranks 31.). Topping the global index: Zurich.

Expensive Bad Habits and No Cheap Dates

The Report extracts its Quality of Life rankings from Numbeo.com, which covers cities large and small all over the world and bases its rankings on a combination of individual indices that include Purchasing Power, Pollution, Safety, and the like.

But the Report also includes its own quirky indexes, like the “Bad Habits Index” (cost of 5 beers and 2 packs of cigarettes), “Cheap Date Index,” and “Men’s Standard Haircut in an Expat Area Index.” No surprise: San Francisco is expensive under all those metrics. Surprise: San Francisco doesn’t even make the top 54 for (most expensive) Five Star Hotel Rooms with a View. That honor goes to Milan, Madrid, and Vienna in that order. Another surprise: San Francisco ranks third most expensive under Monthly Internet Service, behind Dubai and Dublin. Thank you, Silicon Valley!

But Lots of Income

One of the major takeaways of the Report: San Francisco tops the charts for both Monthly Income (after taxes) and Monthly Disposable Income After Rents. It’s jumped 7 and 21 places, respectively, in just the last 5 years. So, while it’s expensive to rent here, it seems that incomes have more than kept up the pace – though I can’t think of anyone who feels that way.

Boom or Gloom?

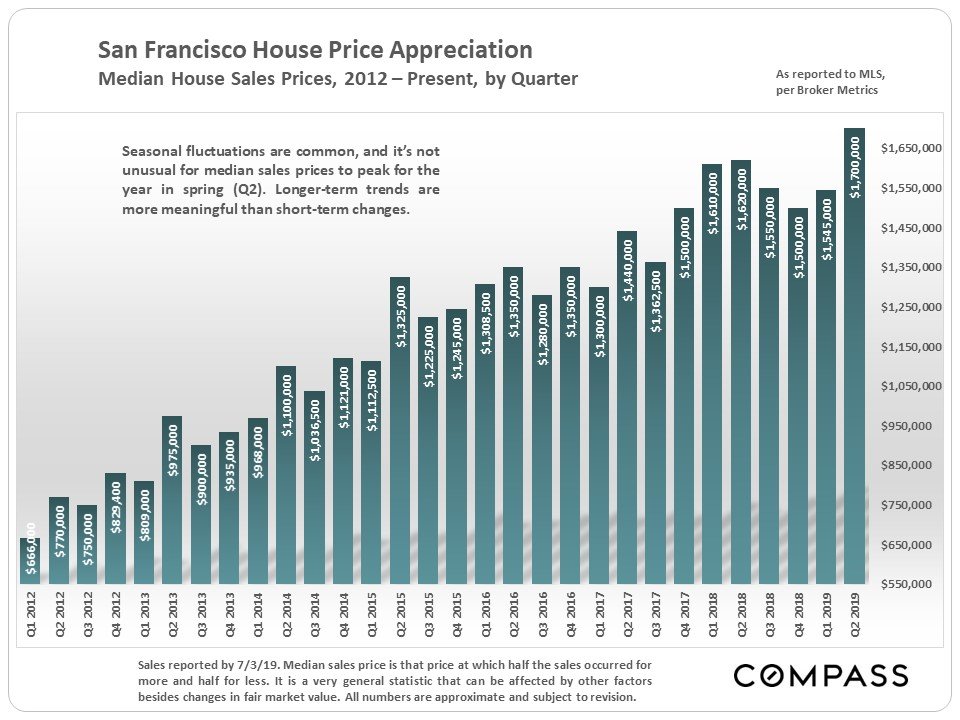

With San Francisco real estate prices recently hitting new highs (see chart below), people often ask me where I see the real estate market going. That’s particularly true now, with so much volatility in the stock market, not to mention underlying geo-political concerns like Brexit, the trade war with China, and oil supplies coming out of the Straits of Hormuz.

Alas, I have no crystal ball. But our global ranking is a good part of the reason why I feel bullish about San Francisco in the long-term. We are a global city, blessed by a thriving and diversified economy; an educated work-force; stunning scenery; and a decent climate (except right now!). While we aren’t immune from economic downturns, there’s every reason to expect that people will continue to want to live and work here – despite the expense and challenges – for the foreseeable future.

As always, your questions, comments and referrals are much appreciated!

You can find the full article here at The Atlantic. Their choice of

You can find the full article here at The Atlantic. Their choice of

Just a few days ago, The San Francisco Business Times

Just a few days ago, The San Francisco Business Times